Do you think your home is safe from flooding just because it sits outside a high-risk zone? Have you wondered, “Do I need flood insurance if I’m not in a flood zone in Bluffton?”

Many homeowners assume they’re protected — yet roughly 20–25% of flood claims come from properties outside high-risk areas. And standard homeowners insurance does not cover flood damage caused by rising water.

Let’s take a clear look at your actual risk — and whether flood insurance makes sense for your home.

The question isn’t whether flooding is possible — it’s whether you’re financially prepared if it happens.

Key Takeaways

Flood insurance may still be important even if you do not live in a high-risk flood zone. A meaningful percentage of claims come from lower-risk areas.

Regular homeowners insurance does not cover flood damage caused by rising water. You need a separate flood insurance policy for that protection.

Flood risk is not limited to mapped high-risk zones. Heavy rain, storm surge, tidal flooding, and drainage issues can impact homes in moderate- and low-risk areas.

What Does “Not in a Flood Zone” Mean for Flood Insurance?

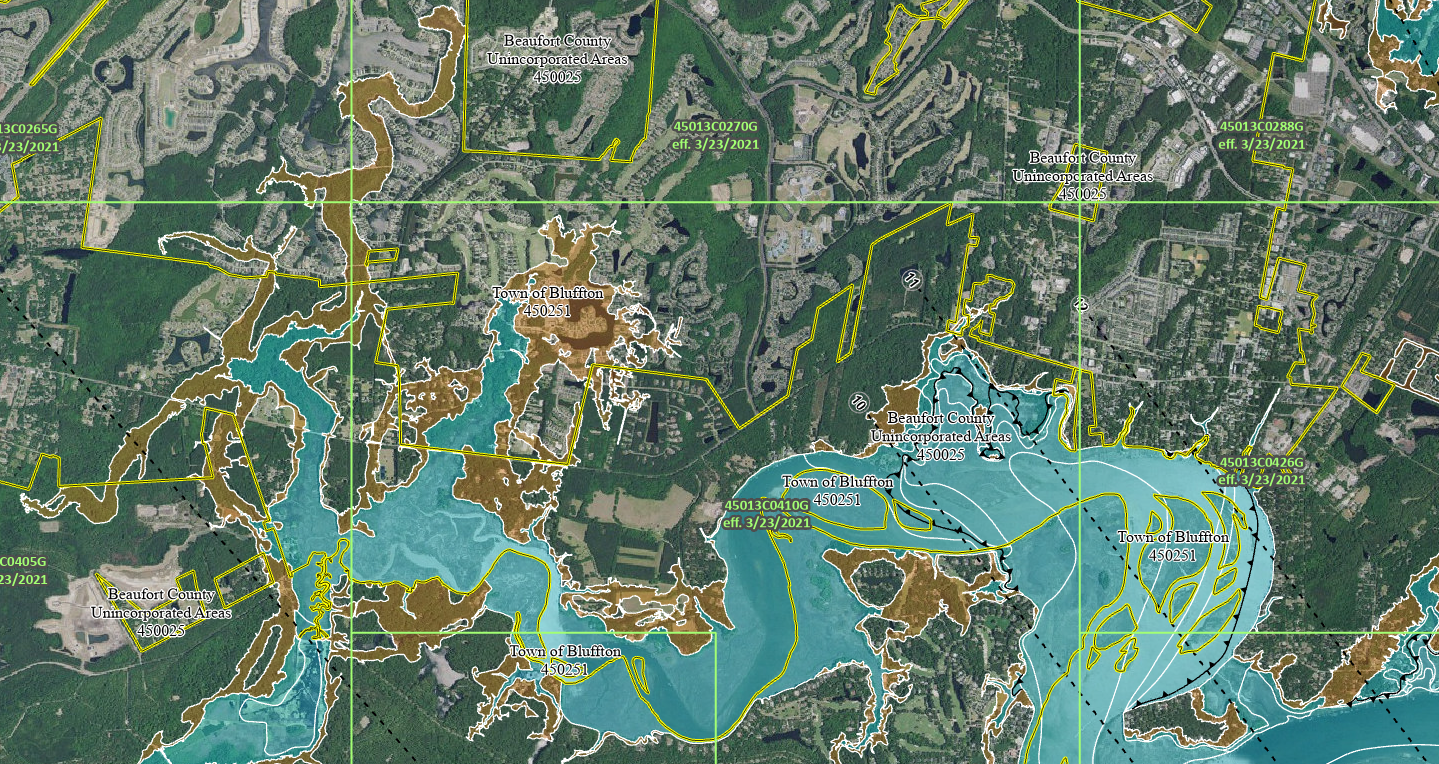

How FEMA Flood Zones Are Determined

FEMA creates flood maps to estimate the likelihood of flooding in specific areas. These maps are based on historical flood data, elevation studies, rainfall patterns, and modeling.

Properties are typically categorized as high-risk, moderate-risk, or minimal-risk. The most significant high-risk areas are known as Special Flood Hazard Areas (SFHAs).

What Are Special Flood Hazard Areas (SFHAs)?

SFHAs are areas with the highest statistical probability of flooding. If your home is located in one of these zones, it has a 1% annual chance of flooding — commonly referred to as the “100-year floodplain.”

If you have a mortgage and your property is in an SFHA, your lender will usually require flood insurance.

High-, Moderate-, and Low-Risk Flood Zones Explained

Flood Zone Type | Description |

|---|---|

High risk flood zone | Areas with a 1% annual chance of flooding, known as the ‘100-year floodplain’. |

Moderate flood hazard zone | Properties between the 100-year and 500-year floodplains, with a lower but existing flood risk. |

Minimal flood hazard zone | Areas outside the 500-year floodplain, experiencing very limited flooding and few restrictions. |

Many homes in Bluffton, Hilton Head, and Beaufort County fall into moderate or minimal risk zones. While the statistical risk may be lower, flooding still occurs in these areas.

Flood zones measure probability — not certainty.

Flood maps show how likely flooding is based on past data. They do not guarantee what will happen in the future. Heavy rainfall, storm surge, blocked drainage systems, and development changes can all increase localized risk.

Bold Takeaway: Flood zone maps measure risk, but they do not guarantee protection from flooding.

Risk vs. Guarantee: The Common Misunderstanding

One of the biggest misconceptions homeowners have is this:

“If I’m not in a high-risk flood zone, I don’t need flood insurance.”

That assumption is not always accurate.

A significant portion of flood claims come from properties outside high-risk zones. In the Lowcountry, heavy rain events, new development, and drainage challenges have caused flooding in neighborhoods not designated as high-risk.

Being outside a high-risk flood zone does not eliminate flood risk.

Flood maps are tools. They are not promises.

They rely on historical records and modeling, which may not fully reflect:

Updated development patterns

Drainage limitations

Changing weather patterns

Localized runoff issues

Limitations of FEMA Flood Mapping

Limitation | Description |

|---|---|

Outdated or incomplete data | May not reflect current development or recent flooding events. |

Localized flooding issues | Urban drainage or stormwater failures may not appear on official maps. |

False sense of security | Zone X homeowners may underestimate real exposure. |

Flooding does not follow property lines — and it does not stop at mapped boundaries.

Bold Takeaway: You should not rely on flood zone maps alone to decide whether you need flood insurance.

If you’d like to better understand how flood policies work, you can review our guide comparing NFIP and private flood insurance options. You may also want to explore what standard homeowners insurance excludes so you understand where coverage gaps exist.

Can You Still Need Flood Insurance Outside High-Risk Areas?

Why Homes Outside Flood Zones Still Flood

Living outside a high-risk flood zone does not eliminate exposure to water damage. In coastal communities like Bluffton, Hilton Head, and Beaufort County, flooding can occur for several reasons that have nothing to do with FEMA zone designations.

Heavy Rainfall Overwhelming Drainage Systems

Lowcountry storms can drop several inches of rain in a short period of time. When storm drains and retention systems cannot keep up, water backs up into streets, yards, and sometimes homes.

Even properties in moderate- or minimal-risk zones can experience flooding during intense rainfall events.

Storm Surge and Tidal Flooding

Coastal proximity adds another layer of exposure. Storm surge from hurricanes and tropical systems can push water inland well beyond mapped flood boundaries. In addition, high tides — especially king tides — can temporarily flood roads and low-lying properties.

Many homes in Beaufort County sit only a few feet above sea level. Even if your property is not in a high-risk FEMA zone, tidal and surge-related flooding can still impact your home.

Flood risk along the coast is not limited to hurricanes.

Rapid Development and Runoff Changes

As Bluffton and surrounding areas continue to grow, development changes how water moves. Paved surfaces prevent rainwater from soaking into the ground, increasing runoff and redirecting flow into new areas.

Aspect | Description |

|---|---|

Stormwater management objective | Reduce flooding by properly managing runoff after construction. |

Best Management Practices (BMPs) | Systems designed to slow, capture, and redirect stormwater. |

Maintenance requirements | Regular upkeep is essential to keep drainage systems functioning properly. |

When stormwater systems are not properly maintained — or when runoff exceeds design capacity — localized flooding can occur.

Blocked Storm Drains and Infrastructure Issues

Flooding does not always require a major storm. Leaves, debris, or poorly maintained drainage systems can cause water to accumulate quickly.

Even a short but intense rain event can lead to property damage if water has nowhere to go.

A meaningful percentage of flood insurance claims — often estimated at 20–25% — come from properties outside high-risk zones. That statistic alone is a reminder that flood maps do not eliminate exposure.

And remember: standard homeowners insurance does not cover damage caused by rising water.

Bold Takeaway: Flood risk exists beyond high-risk map lines — and homeowners insurance will not cover rising water damage.

If you want a clearer understanding of what your current policy does and does not cover, review our guide on homeowners insurance exclusions. You can also explore the differences between NFIP and private flood insurance policies to see what options are available.

If you’d like to talk through your specific situation, we’re happy to help you evaluate your risk and determine whether flood insurance makes sense — without pressure.

Why Homeowners Insurance Does Not Replace Flood Insurance

Many homeowners assume their policy covers any type of water damage. Unfortunately, that’s not the case.

Standard homeowners insurance does not cover flood damage caused by rising water. If water enters your home from outside — whether from heavy rainfall, storm surge, or an overflowing river — it is typically excluded.

What Homeowners Insurance Usually Does Not Cover

Exclusion Type | Description |

|---|---|

Flood damage | Rising water from outside the home is excluded. |

Storm surge | Treated as flood damage under most policies. |

Surface water runoff | Water accumulating outside and entering the home is excluded. |

Sewer backup (without endorsement) | Often excluded unless specifically added to the policy. |

It’s important to review your policy carefully so you understand where gaps may exist.

What Qualifies as a “Flood” Under Insurance Policies?

Flood insurance policies — including those backed by the National Flood Insurance Program (NFIP) — define a flood as:

A general and temporary condition where two or more properties, or two or more contiguous acres of normally dry land, are inundated by water or mudflow.

Covered events typically include:

Overflow of inland or tidal waters

Rapid accumulation or runoff of surface water

Storm surge

Mudflow caused by water

If rising water affects multiple properties or large areas of land, it generally qualifies as a flood under insurance definitions.

Bold Takeaway: Flood insurance covers events that standard homeowners insurance specifically excludes.

The Financial Risk of Assuming You’re Covered

One of the most costly insurance mistakes homeowners make is assuming coverage exists when it does not.

Without flood insurance:

You may be responsible for structural repairs out of pocket

Personal belongings damaged by floodwater may not be covered

Savings may be used for recovery instead of future plans

Flood damage can be expensive — and financial recovery without proper coverage can take years.

Bold Takeaway: It’s far better to clarify your coverage now than discover a gap after a loss.

If you’d like a clearer breakdown of what your homeowners policy does and does not include, review our homeowners insurance coverage guide.

How Much Does Flood Insurance Cost Outside High-Risk Zones?

For many homeowners, cost is the deciding factor.

The good news: flood insurance is often significantly more affordable outside high-risk zones.

What Impacts Flood Insurance Premiums?

Several factors determine your premium:

Flood Zone Designation

Homes outside high-risk zones typically have lower premiums.

Elevation

Properties built above Base Flood Elevation (BFE) generally qualify for better rates.

Foundation Type

Elevated homes on pilings or crawlspaces often cost less to insure than slab foundations.

Coverage Limits

Higher coverage amounts increase premiums, but also provide stronger protection.

Replacement Cost vs. Actual Cash Value

Replacement cost provides fuller reimbursement but costs more than actual cash value coverage.

Bold Takeaway: Flood insurance in moderate- or low-risk zones is often more affordable than homeowners expect.

Typical Premium Ranges

Risk Zone | Estimated Premium Range |

|---|---|

Low-risk (Zone X) | Often $500–$700 annually |

Moderate-risk | Mid-hundreds to low thousands |

High-risk (SFHA) | $1,500–$3,000+ depending on property |

Premiums vary based on property characteristics, but coverage outside high-risk zones is generally less expensive.

If you’d like to compare NFIP and private flood insurance options, reviewing the differences can help you choose the right fit.

Flood Insurance Risks in Bluffton, Hilton Head, and Beaufort County, SC

Living in the Lowcountry means understanding coastal risk beyond FEMA map lines.

Coastal Exposure and Storm Surge

Bluffton, Hilton Head, and Beaufort County sit near tidal creeks, marshland, and the Atlantic Ocean. Storm surge can push water inland during hurricanes or tropical systems — sometimes beyond mapped high-risk zones.

Factor | Why It Matters |

|---|---|

Flood zone designation | Indicates statistical probability, not certainty. |

Elevation above BFE | Higher elevation generally reduces both risk and premium. |

Marshland protection | Natural buffers help, but do not eliminate surge exposure. |

Bold Takeaway: Coastal location alone increases flood exposure, regardless of zone classification.

Heavy Rainfall and Flash Flooding

Lowcountry storms can produce intense rainfall in short periods. When drainage systems reach capacity, water accumulates quickly.

Even properties outside high-risk zones can experience flooding during severe rain events.

High Tides and King Tides

Tidal flooding has become more frequent in coastal communities. During king tides, water levels rise significantly — sometimes flooding roads and low-lying areas without rainfall.

This exposure exists independent of FEMA flood mapping.

Growth and Drainage Challenges

Rapid development changes water flow patterns. Increased pavement and construction redirect runoff into new areas. Many stormwater systems require ongoing maintenance to function properly.

Localized drainage limitations are rarely reflected fully in FEMA maps.

Bold Takeaway: Local development and coastal conditions create real flood exposure, even outside high-risk zones.

For more on protecting coastal homes, review our coastal home insurance guide.

Pros and Cons of Buying Flood Insurance Voluntarily

Pros

Financial Protection

Flood repairs can be costly. Insurance provides structured financial recovery instead of relying on savings.

Lower Premiums Outside High-Risk Zones

Moderate- and low-risk homeowners often secure coverage at more affordable rates.

Reduced Financial Uncertainty

Having flood insurance can reduce stress during hurricane season and major storm events.

Increased Buyer Confidence

Documented coverage can provide reassurance to future homebuyers.

Bold Takeaway: Voluntary flood insurance offers meaningful protection at a relatively modest cost in lower-risk zones.

Cons

Additional Annual Expense

It adds an additional annual premium, which may feel unnecessary if you’ve never experienced flooding.

Perceived Low Risk

Some homeowners choose to self-insure because flooding has not occurred previously.

Coverage Limits

Policy limits may not cover every improvement or high-end finish without customization.

Bold Takeaway: The decision ultimately comes down to your comfort with financial risk.

How to Decide If Flood Insurance Makes Sense for You

The decision is personal and financial.

Ask yourself:

Could you comfortably repair your home after a flood without insurance?

Would replacing damaged furniture and belongings strain your finances?

How would a $20,000–$50,000 unexpected expense impact your plans?

Some homeowners prefer transferring that risk to an insurance policy. Others choose to assume it.

Approach | Outcome |

|---|---|

Proactive | Purchase coverage now and reduce uncertainty. |

Reactive | Wait and potentially absorb the financial impact later. |

Bold Takeaway: Flood insurance shifts uncertainty from your savings to a policy.

Final Thoughts

Living outside a mapped high-risk flood zone does not eliminate flood exposure. Standard homeowners insurance will not cover rising water damage. And a meaningful portion of claims come from moderate- and low-risk areas.

Flood insurance is ultimately a risk management decision.

If you’re unsure whether it makes sense for your home in Bluffton, Hilton Head, or Beaufort County, we’re happy to review your current coverage and walk through your options with you — clearly and without pressure.

That way, you can make a confident, informed decision about protecting your home.

FAQ

Do you need flood insurance if your lender does not require it?

Yes, you still need it. Floods can happen anywhere, even if your lender does not ask for it. Flood insurance helps protect your home and your money. You make the choice to stay safe, not your lender.

Bold Takeaway: You are in charge of your protection, not your lender.

Will flood insurance cover damage from heavy rain or storm surge?

Yes, it will. Flood insurance pays for damage from rising water, heavy rain, and storm surge. Homeowners insurance does not pay for these things.

Can you buy flood insurance if you are not in a high-risk zone?

Yes, you can buy it in any zone. Flood insurance is often cheaper outside high-risk areas. This means you can get good protection for less money.