Quick Summary

This article explains that the labeled lifespan of 20-year, 30-year, and 50-year roof shingles refers to warranty coverage, not the actual performance or lifespan of the roof. It clarifies how real-world factors affect roof longevity and how insurance companies evaluate roofs based on age and condition rather than shingle ratings. Readers will learn why shingle warranties don’t guarantee roof life and how insurance coverage changes as roofs age.

Key Takeaways:

- Shingle lifespan labels indicate warranty periods for manufacturing defects, not the actual duration your roof will last under normal conditions.

- Most roofs wear out sooner than their labeled lifespan due to weather, installation quality, and maintenance factors.

- Insurance companies assess roofs based on their age and condition, often valuing older roofs at depreciated costs rather than full replacement.

- Choosing shingles should depend on how long you plan to stay in your home, not solely on the warranty length printed on the packaging.

What do 20-year, 30-year, and 50-year roof shingles really mean? And more importantly—how long will your roof actually last?

If you’ve ever assumed a “30-year roof” would last 30 years, you’re not alone. But here’s the reality: many homeowners are surprised to find their roof doesn’t perform—or get evaluated by insurance—the way they expected.

In fact, you might think you’re buying a 30-year roof… until your insurance company evaluates it like a 15-year one.

In this article, we’ll break down what these shingle ratings actually mean, how long they last in real-world conditions, and how insurance companies truly evaluate your roof when it matters most.

The number on your shingles doesn’t determine how long your roof will last—or how insurance will cover it.

Key Takeaways

Shingle lifespan labels reflect warranty coverage—not how long your roof will actually last.

Most roofs fail well before their labeled lifespan due to weather, installation quality, and maintenance.

Insurance companies evaluate your roof based on age and condition—not whether it’s labeled 20-, 30-, or 50-year shingles.

As your roof ages, coverage often shifts from full replacement (RCV) to depreciated value (ACV), reducing your payout.

The right shingle choice depends on how long you plan to stay in your home—not just the warranty on the packaging.

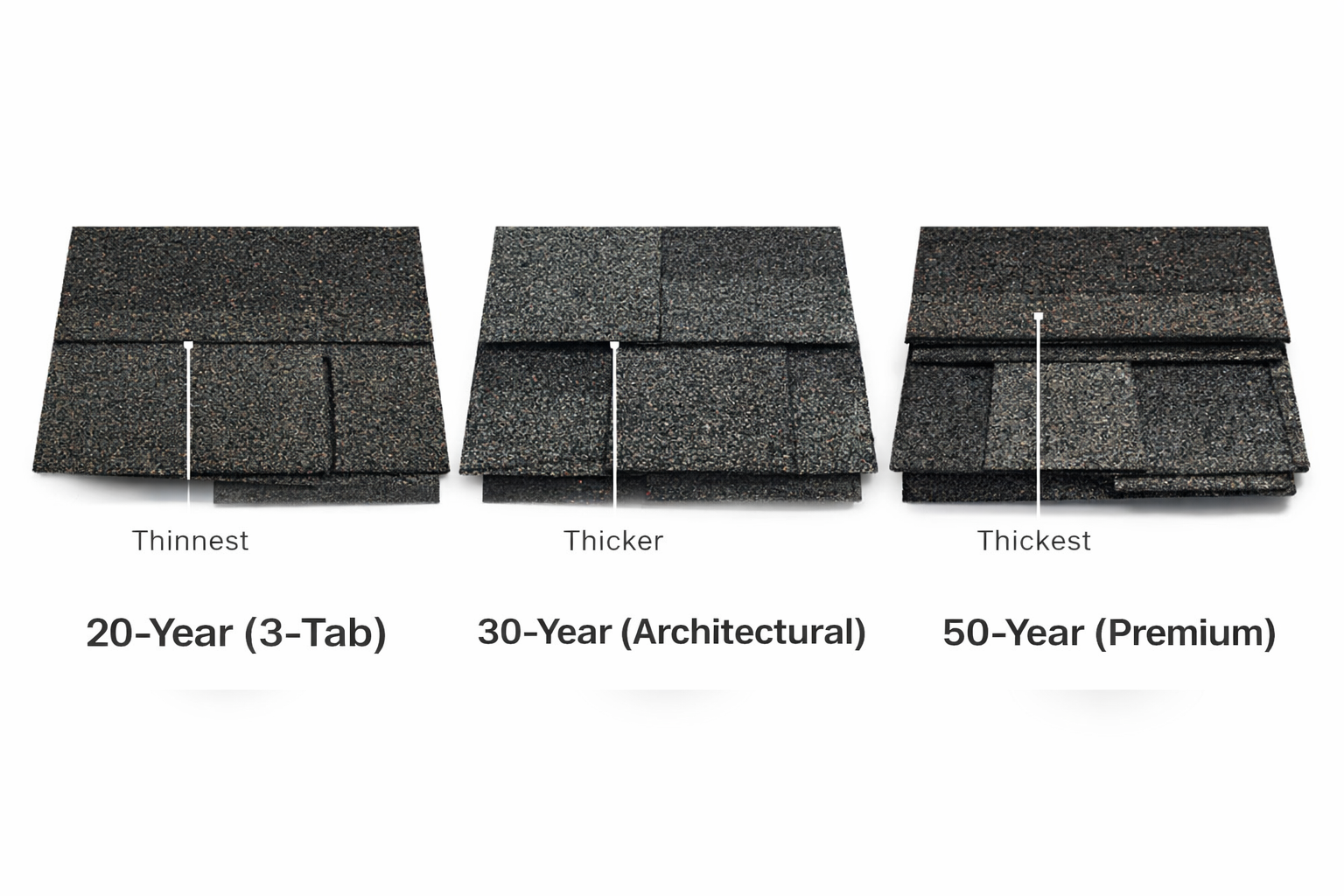

What Do 20-Year, 30-Year, and 50-Year Shingles Mean

Warranty vs. Real Roof Lifespan

Shingle lifespan labels reflect warranty coverage—not how long your roof will actually last.

Many homeowners assume a 20-, 30-, or 50-year shingle will last exactly that long. In reality, those numbers refer to how long the manufacturer will cover defects—not how long your roof will perform.

Most warranties only cover manufacturing defects. They typically do not include:

Storm damage

Installation issues

Normal wear and aging

And in many cases, coverage decreases over time.

For example, a 30-year shingle may only be fully covered for the first 10 years. After that, the coverage is prorated—meaning the older your roof gets, the less the manufacturer will pay.

Even with 50-year shingles, extended coverage does not mean extended performance.

The warranty period is about liability—not lifespan.

Shingle Types and Materials

Not all shingles are built the same—and that directly impacts how long your roof will last.

In general, shingle categories reflect differences in thickness, material quality, and design:

20-year shingles: Basic 3-tab design, thinner, lower-cost, shorter lifespan

30-year shingles: Thicker architectural shingles with better durability

50-year shingles: Premium, multi-layered shingles designed for higher resistance to weather

Architectural and premium shingles (30- and 50-year categories) typically last longer because they are thicker and more durable—not because of the number on the label.

Installation quality and ventilation play just as big a role as the materials themselves.

Higher-quality shingles can last longer—but only if they’re installed and maintained properly.

How Long 20-, 30-, and 50-Year Shingles Actually Last

Most roofs fail well before their labeled lifespan.

While shingles are labeled for 20, 30, or 50 years, real-world performance looks more like this:

20-year shingles: ~12–17 years

30-year shingles: ~18–25 years

50-year shingles: ~25–35 years

These ranges vary based on climate, installation, and maintenance. Harsh sun, high winds, hail, and poor ventilation can all shorten a roof’s lifespan.

Even under ideal conditions, it’s uncommon for asphalt shingles to reach their full labeled lifespan.

Real-world conditions—not labels—determine how long your roof lasts.

Why 50-Year Roof Shingles Rarely Last 50 Years

Manufacturer Warranties vs. Real-World Performance

A “50-year” shingle is a warranty category—not a realistic expectation for lifespan.

While 50-year shingles are built to be more durable, they are still affected by real-world conditions that shorten their life. Sun exposure, temperature swings, humidity, hail, and high winds all contribute to wear over time.

Even in good conditions, most asphalt shingles fall well short of their labeled lifespan.

What the Warranty Fine Print Actually Says

Shingle warranties are designed to limit manufacturer liability—not guarantee long-term performance.

Most warranties include important limitations that homeowners often overlook:

Installation errors are not covered

Lack of maintenance can void coverage

Storm damage and extreme weather are typically excluded

In addition, many warranties are prorated—meaning coverage decreases as your roof ages.

Real-World Factors That Shorten Lifespan

Most roofs fail early due to a combination of installation quality, environment, and maintenance—not product defects.

Common factors that reduce the lifespan of 50-year shingles include:

Improper installation (especially poor nailing or flashing)

Inadequate attic ventilation

Prolonged sun exposure and heat buildup

Severe weather like wind and hail

Lack of routine maintenance

Even the highest-quality shingles won’t reach their full lifespan if these factors aren’t managed properly.

Real-world conditions—not warranty labels—determine how long your roof actually lasts.

How Insurance Companies Actually Evaluate Your Roof

How Insurance Views Roof Age

Insurance companies evaluate your roof based on age and risk—not the label on your shingles.

As your roof gets older, it becomes more likely to fail. Because of that, insurers pay close attention to how many years your roof has been in place—not whether it was labeled as a “30-year” or “50-year” product.

In many cases:

Roofs over 10–15 years may begin losing full replacement coverage

Roofs over 20 years are often limited to actual cash value (ACV)

Roofs over 25 years may be denied coverage altogether unless they’ve been recently replaced

Why Insurance Doesn’t Care About Shingle “Years”

Insurance companies do not base coverage decisions on whether your shingles are labeled 30-year or 50-year.

They understand that real-world conditions—weather, installation quality, and maintenance—have a much bigger impact on how a roof performs over time.

Instead of relying on product labels, insurers evaluate:

The current condition of your roof

Visible wear, damage, or deterioration

The likelihood of future claims

Insurance companies assess risk—not marketing claims.

Roof Condition and Coverage

Your roof’s condition matters more than the type of shingles you installed.

Insurance companies often inspect roofs for:

Missing or damaged shingles

Signs of leaks or water intrusion

Poor installation or previous repairs

If your roof shows signs of wear or neglect, your coverage may be reduced—or denied altogether.

Keeping records of maintenance and repairs can improve your chances of receiving full coverage.

RCV vs. ACV Policies Explained

The type of insurance policy you have can significantly impact how much you’re paid for a roof claim.

Replacement Cost Value (RCV): Covers the full cost to replace your roof without deducting for age or wear

Actual Cash Value (ACV): Pays only the depreciated value of your roof, meaning older roofs receive significantly less

For example, if your roof is 18 years old, an ACV policy may only cover a portion of the replacement cost—leaving you to pay the rest out of pocket.

As your roof ages, your payout typically decreases—even if your shingles were labeled for a longer lifespan.

Choosing Between 20-, 30-, and 50-Year Shingles

The right shingle choice depends on how long you plan to stay in your home, your budget, and how much risk you’re willing to take on.

Best Option If You Plan to Stay Long-Term

If you plan to stay in your home for 10+ years, investing in higher-quality shingles usually makes sense.

30-year and 50-year shingles offer:

Better durability

Improved resistance to weather

Longer realistic lifespan compared to basic options

However, it’s important to understand that even premium shingles rarely last their full labeled lifespan. What you’re really paying for is better performance—not a guaranteed number of years.

Best Option If You Might Sell Soon

If you’re planning to sell within the next few years, your goal is different.

You want a roof that:

Looks good to buyers

Passes inspection

Reduces concerns about near-term replacement

In most cases, a newer roof with 30-year architectural shingles strikes the right balance between cost and perceived value.

Buyers care more about the age and condition of the roof than the specific label.

Best Option If You’re Budget-Conscious

If upfront cost is your main concern, 20-year (3-tab) shingles are the most affordable option.

They can make sense if:

You don’t plan to stay long

You need a short-term solution

You’re managing a tight budget

Just keep in mind:

They typically wear out faster

They may require replacement sooner

Insurance limitations may come into play earlier

Final Thought on Choosing the Right Shingles

There is no “best” shingle—only the best choice for your situation.

The biggest mistake homeowners make is choosing based on the label alone. Instead, focus on:

How long you’ll stay in the home

The quality of installation

How your roof will be viewed by insurance over time

Because in the end, your roof’s performance—and your coverage—will depend far more on those factors than the number printed on the packaging.

Frequently Asked Questions

How do I know when my roof needs to be replaced?

Common warning signs include missing or curling shingles, leaks, dark streaks, and granules collecting in your gutters. However, visible damage isn’t the only indicator.

If your roof is over 15–20 years old, it’s worth having it professionally inspected—even if it looks fine from the ground. Many roofing issues develop gradually and aren’t obvious until they become costly.

If your roof is aging, don’t wait for a leak—get it evaluated before it becomes an insurance or repair issue.

Does a 30-year shingle guarantee 30 years of coverage?

No. The “30-year” label refers to a manufacturer warranty for defects—not a guarantee of how long your roof will last or how long insurance will cover it.

In real-world conditions, most 30-year shingles last closer to 18–25 years depending on climate, installation, and maintenance.

A 30-year shingle is a warranty category—not a promise of performance.

Will my insurance cover my old roof?

It depends on your roof’s age, condition, and your policy type.

Many insurance companies begin limiting coverage once a roof reaches 15–20 years old. Older roofs are often covered under Actual Cash Value (ACV), meaning depreciation reduces your payout. In some cases, coverage may be denied altogether.

Insurance companies evaluate risk based on age and condition—not the label on your shingles.

What is the difference between RCV and ACV insurance policies?

Replacement Cost Value (RCV) covers the full cost to replace your roof without deducting for age or wear

Actual Cash Value (ACV) only pays the depreciated value, meaning older roofs receive significantly less

For example, an older roof may only be partially covered under ACV, leaving you responsible for the remaining cost.

As your roof ages, your payout typically decreases—even if your shingles were labeled for longer.

Can I extend my roof’s life?

Yes—while you can’t control everything, proper maintenance can significantly extend your roof’s lifespan.

Key steps include:

Scheduling regular inspections

Keeping gutters clean

Addressing small issues before they become major problems

Ensuring proper attic ventilation

Consistent maintenance won’t guarantee lifespan—but it can delay costly repairs and replacement.

See Also

Understanding Gap Insurance: The $8,000 Importance You Overlook