Quick Summary

This article explains how home insurance deductibles work, including the difference between flat dollar and percentage-based deductibles, and how disaster-specific deductibles like those for hurricanes affect your out-of-pocket costs. It highlights the importance of understanding your deductible type, saving money for it, and knowing that flood and earthquake damage require separate insurance policies.

Key Takeaways:

- A deductible is the amount you pay first before insurance covers the rest, and it can be a fixed dollar amount or a percentage of your home’s insured value.

- Percentage-based deductibles are common for disasters like hurricanes and can be significantly higher than regular deductibles, increasing your out-of-pocket costs.

- Flood and earthquake damages are not covered by standard home insurance and require separate policies with their own deductibles.

- Review your insurance policy annually and save money for your deductible to avoid surprises and handle claims smoothly.

When disaster happens, your deductible tells you what you pay first before insurance helps. You do not want surprises with your insurance. Knowing how your home insurance works helps you not feel confused. How Your Home Insurance Deductible Works When Disaster Strikes is important for your money and your peace of mind.

Key Takeaways

Your deductible is what you pay first before insurance helps. It can be a set dollar amount or a percent of your home’s value.

Some disasters like hurricanes have higher deductibles that use percentages. Floods and earthquakes need their own insurance policies.

Check your policy every year. Save money for your deductible. Know your coverage to avoid surprises and handle claims easily.

How Home Insurance Deductibles Work

What Is a Deductible?

You may wonder what a deductible means when you make a claim. A deductible is money you pay first before insurance pays the rest. For example, if a storm causes $10,000 in damage and your deductible is $1,000, you pay $1,000. The insurance company pays the other $9,000. You pick your deductible when you buy your policy. Most deductibles are between $500 and $2,500, but some are more. Deductibles are used for each claim, like fire, theft, or wind damage. They usually do not count for liability claims.

Flat vs. Percentage Deductibles

Let’s look at the two main types of deductibles:

A flat dollar deductible is a set amount, like $1,000. If you have $8,000 in damage, you pay $1,000 and insurance pays $7,000.

A percentage-based deductible is a percent of your home’s insured value. For example, if your home is insured for $300,000 and your deductible is 2%, you pay $6,000 before insurance helps. These are common in places with lots of storms.

Tip: If you pick a higher deductible, your monthly bill can be lower. But you need to save money in case you need to file a claim.

Disaster-Specific Deductibles

Some disasters have their own special deductibles. In coastal South Carolina, you might see hurricane or wind/hail deductibles. These are often percentage-based and much higher than your regular deductible. For example, a hurricane deductible could be 5% of your home’s insured value. Flood and earthquake damage are not covered by standard home insurance. You need separate policies for those, each with their own deductible.

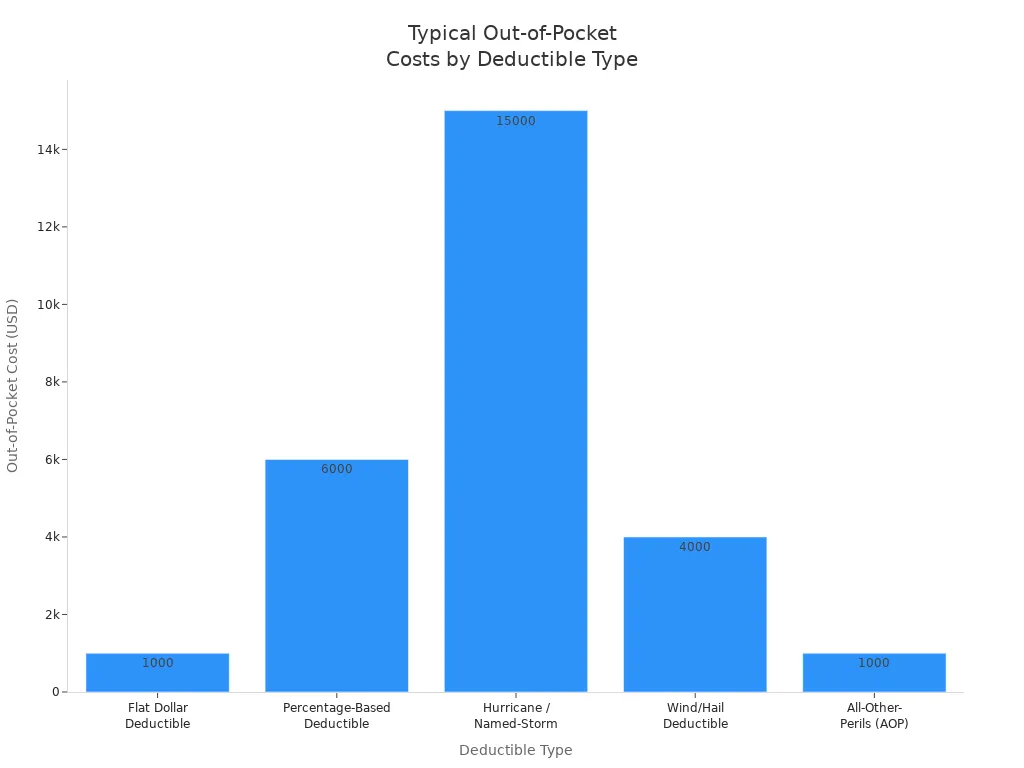

Deductible Type | Example Out-of-Pocket Cost | |

|---|---|---|

Fire | Flat dollar | $1,000 on $10,000 claim |

Hurricane | Percentage (5%) | $15,000 on $300,000 home |

Wind/Hail | $4,000 on $200,000 home | |

Flood | Separate policy | Varies by policy |

Earthquake | Percentage (2%-20%) | $6,000+ on $300,000 home |

Examples

Let’s see how deductibles work in real life. Imagine a hurricane hits Hilton Head. Your home is insured for $300,000 and your hurricane deductible is 5%. You would pay $15,000 before insurance pays anything. For a fire claim with a $1,000 flat deductible, you pay $1,000 and insurance covers the rest. Many people think they have a $1,000 deductible for everything, but disaster deductibles can be much higher.

Knowing how deductibles work helps you get ready for emergencies and avoid surprises.

How Your Home Insurance Deductible Works When Disaster Strikes

Covered and Excluded Disasters

You might think your home insurance covers every disaster. That is not always true. It is important to know what your policy covers. This helps you avoid surprises when you need help. Here is a quick look at which disasters are usually covered and which are not:

Disaster Type | Covered by Standard Home Insurance? | Notes and Exceptions |

|---|---|---|

Windstorms and Hail | Yes | This includes thunderstorms, tornadoes, and hurricanes (wind/hail only). |

Lightning | Yes | It covers fire and electrical surges. |

Wildfires | Yes | Fire and smoke damage are included. |

Fire | Yes | It covers damage to your home and your things. |

Explosion | Yes | Accidental explosions are covered. |

Extreme Cold (Ice, Snow, Winter Storms) | Yes | Burst pipes, ice dams, and heavy snow damage are covered. |

Tornadoes | Yes | Wind, hail, and debris damage are covered. Flooding is not. |

Hurricanes (Wind and Hail) | Yes | Wind and hail damage are covered. Flooding from hurricanes is not. |

Flooding | No | You need separate flood insurance. |

Earthquakes | No | You need separate earthquake insurance. |

Sinkholes | No | These are usually not covered. Check with your insurer. |

Tip: Floods, earthquakes, and sinkholes are not covered by most standard home insurance policies. You need separate policies for these disasters.

If you live near the coast in South Carolina, you may face hurricane and wind risks. Your policy may have special deductibles for these events. Always check your policy to see how your home insurance deductible works when disaster strikes. Some disasters, like hurricanes, may have a percentage-based deductible. This can be much higher than your regular flat deductible.

Claim Process

When disaster happens, you want to know how your home insurance deductible works when disaster strikes. Here is a simple step-by-step guide to help you with claims:

Stay Safe: Make sure you and your family are safe first.

Document the Damage: Take photos and videos of all damage. Write down what happened and what was damaged.

Contact Your Insurance Company: Call your insurance provider as soon as you can. Give them your policy number and a short description of the damage.

Review Your Policy: Look at your policy to see what is covered and what your deductible is for this disaster. Remember, hurricane or wind/hail deductibles may be higher than your regular deductible.

File Your Claim: Send your claim with all the information and photos you collected.

Meet the Adjuster: An insurance adjuster will visit your home to look at the damage. Show them everything and give them your receipts or repair estimates.

Make Temporary Repairs: Stop more damage by making quick fixes, like covering broken windows. Keep your receipts for these repairs.

Track Everything: Write down every call, email, or letter with your insurance company. This helps if there are any problems later.

Get Paid and Start Repairs: Once your claim is approved, you will get your payment. You can then start fixing your home.

Note: If your claim is denied, ask why. You can appeal or give more information if needed.

Knowing how your home insurance deductible works when disaster strikes makes the claims process less stressful. You will know what to expect and what you need to pay out of pocket.

Managing Your Deductible

You can take steps now to get ready for disasters. Here is how your home insurance deductible works when disaster strikes and how you can manage it:

Review Your Policy Every Year: Your home’s value and your deductible can change. Check your policy each year with your insurance agent. This helps you understand your deductible and avoid surprises.

Know Your Deductible Types: Some disasters, like hurricanes, have percentage-based deductibles. For example, a 2% hurricane deductible on a $300,000 home means you pay $6,000 before insurance helps. Many people do not know this until they file a claim.

Build an Emergency Fund: Save money to cover your deductible. If you have a higher deductible to save on premiums, make sure you can pay it if you need to file a claim.

Ask About Waiver Provisions: Some policies have a waiver of deductible for large losses. If your claim is very big, your insurance company might not make you pay the deductible at all. This can save you thousands of dollars after a major disaster.

Upgrade Your Home: Make your home stronger against storms and disasters. This can lower your premiums and sometimes your deductible.

Shop Around: Get quotes from different insurance companies. Compare deductibles and coverage to find what works best for you.

Use Trusted Resources: State insurance departments and company websites have guides and tools to help you understand how your home insurance deductible works when disaster strikes.

Tip: If you live in a high-risk area, your deductible may be higher. Always ask your agent to explain your policy and deductible options.

Insurance companies have raised deductibles in recent years, especially for disasters like hurricanes and windstorms. Many homeowners now choose higher deductibles to save on premiums. This means you need to plan ahead so you are not surprised by a big bill after a storm or fire.

Knowing how your home insurance deductible works when disaster strikes gives you peace of mind. You will be ready to handle the claims process and protect your money, no matter what happens.

Knowing your deductible helps you get ready for emergencies. It can also help you not go into debt. Many people have trouble paying after a disaster. Most do not have enough money saved.

In some risky places, deductibles can be as high as $30,000.

Save money for emergencies.

Always be ready for anything.

FAQ

What happens if I can’t pay my deductible after a disaster?

You have to pay your deductible first. Insurance will not help until you do. If you cannot pay, talk to your agent or contractor. They might have ways to help you pay.

Does my deductible change for different disasters?

Yes, it can change for some disasters. Hurricanes often have higher percentage deductibles. Always look at your policy to see what you will owe.

Can I choose my deductible amount?

You get to pick your deductible when you buy insurance. A bigger deductible means you pay less each month. But you will pay more if you make a claim.