Quick Summary

This article explains how an umbrella insurance policy provides extra liability protection beyond standard home and auto insurance, covering costly lawsuits from everyday risks like teen driver accidents, pet bites, and social media issues. It highlights the affordability and broad coverage of umbrella policies, helping readers safeguard their savings and future income from unexpected legal expenses.

Key Takeaways:

- An umbrella policy offers additional liability coverage for large accidents and lawsuits that exceed your home or auto insurance limits.

- Common everyday risks such as teen driver crashes, dog bites, guest injuries, and social media defamation can lead to expensive lawsuits covered by an umbrella policy.

- Umbrella insurance is affordable, often costing less than $1 a day for $1 million in coverage, providing strong financial protection for your household.

- This policy helps pay for legal fees, medical bills, and property damage, protecting all household members from unexpected financial burdens.

Everyday accidents can cost more than you expect. Each year, people file over 100 million lawsuits in state courts. Many of these come from simple mistakes like slips or car crashes. Your regular home or auto insurance might not cover everything. An umbrella policy gives you more protection for a good price. Think about if you feel fully safe.

Key Takeaways

An umbrella policy gives more protection than home and auto insurance. It helps cover big accidents, lawsuits, and legal bills that could take your savings.

Everyday risks like teen driver crashes, social media problems, pet bites, guest injuries, pools, trampolines, and volunteering can cause expensive lawsuits. Umbrella insurance helps pay for these costs.

Umbrella insurance does not cost much. It helps you feel safe by protecting your money and future from surprise bills and legal problems.

1. Umbrella Policy Basics

What It Covers

You want to protect your savings and future income. An umbrella policy gives you extra liability coverage when your home or auto insurance runs out. This policy acts as a safety net. It steps in when a big accident or lawsuit costs more than your regular insurance can pay. You get help with legal bills, medical costs, and property damage. It even covers situations like slander or libel from something you post online.

Here are some common claims an umbrella policy can cover:

Injuries from car accidents with high medical bills.

Lawsuits for defamation or slander from social media.

Accidents at your home, like a guest slipping and falling.

Dog bites or animal attacks.

Injuries at pool parties or from property hazards.

Tip: An umbrella policy also protects all members of your household, not just you.

Why It Matters

You work hard for your money and want to keep it safe. A single lawsuit can threaten your savings, investments, and even your future wages. Standard insurance may not be enough if someone sues you for a large amount. An umbrella policy fills this gap and gives you peace of mind.

Check out how affordable this protection can be:

Coverage Amount | Average Annual Cost (USD) |

|---|---|

$2 million | $225 – $474 |

$5 million | $375 – $608 |

Most families pay less than $1 a day for $1 million in coverage. You get strong protection for a small price. If you want to shield your assets from life’s surprises, an umbrella policy is a smart choice.

2. Teen Drivers

Liability Risk

You want your teen to drive safely. But teens have more accidents than adults. The facts are clear:

Teen drivers ages 16-19 have a fatal crash rate almost three times higher than adults.

In 2022, 811 teen drivers ages 15-18 died in car crashes. There were 2,514 teens involved in deadly crashes.

Drivers ages 15-20 were 8.4% of all drivers in fatal crashes. But they were only 5% of licensed drivers.

Teens ages 16-19 are about four times more likely to crash than older drivers.

Speeding caused almost one-third of deadly crashes with teens.

Even careful families face big risks when teens drive.

Policy Limits

Most families add their teen to the family auto policy. This gives the teen the same liability limits as the rest of the family. States set minimum coverage limits. These limits may not be enough for a bad accident. Here are some examples:

State | Bodily Injury per Person | Bodily Injury per Accident | Property Damage |

|---|---|---|---|

Washington DC | $25,000 | $50,000 | $10,000 |

Virginia (2025) | $50,000 | $100,000 | $25,000 |

If your teen causes a big accident, costs can go over these limits. Medical bills and legal fees add up fast.

Extra Protection

You can protect your family’s money by adding an umbrella policy. This policy helps when accident costs go over your auto insurance. It covers legal defense, medical bills, and damages. You get peace of mind knowing your assets are safe. Even if your teen makes a costly mistake, you are protected. Don’t let one accident put your family’s future at risk. Choose extra protection today.

3. Social Media

Online Liability

People use social media all the time. One post can cause big trouble. Many people get sued for things they share online. Some common problems are:

Libel: writing something false that hurts someone’s reputation

Slander: saying something harmful in a video or audio post

Copyright or brand infringement: using photos or logos without permission

Invasion of privacy: sharing private details or images without consent

Harassment: making repeated or threatening comments

A small mistake online can cost a lot of money. Both teens and adults can face these problems.

Coverage Gaps

Homeowners or renters insurance covers injuries or property damage. It does not help with online defamation or cyberbullying. It also does not cover privacy claims. If your child posts a rumor or shares private photos, your policy will not help. You need a Personal Injury Endorsement for this kind of coverage. Without it, you must pay all legal costs and damages. Many families do not know about this gap until it is too late.

Note: Lawsuits from social media can mean high legal bills, settlements, and even judgments against you.

Umbrella Policy Solution

An umbrella policy can help protect your family. It covers claims for libel, slander, defamation, and invasion of privacy. It pays for legal fees, settlements, and judgments if your regular policy is not enough. For example, if your teen joins a viral challenge that causes harm, umbrella insurance helps. If someone sues you for a hurtful post, you have extra protection. You can feel safe knowing you are covered online.

4. Pets

Animal Incidents

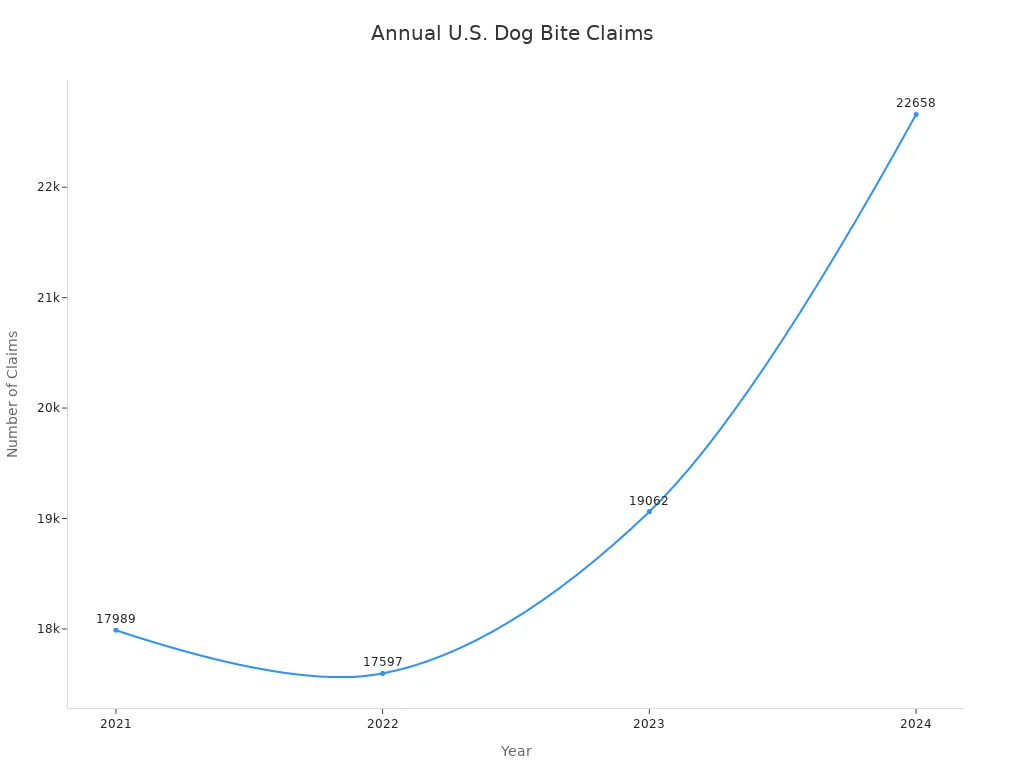

Your pet brings joy to your home, but even the friendliest dog can bite or scratch. Pet-related injuries happen more often than you think. In the United States, dog bite claims have surged in recent years:

Year | Number of Dog Bite Claims in the U.S. | Percentage Change |

|---|---|---|

2021 | 17,989 | N/A |

2022 | 17,597 | -2.2% from 2021 |

2023 | 19,062 | Increase from 2022 |

2024 | 22,658 | +19% from 2023; +48% over past decade |

A single bite can lead to a lawsuit. The average payout for a dog bite claim reached about $58,500 in 2023 and jumped to $69,272 in 2024. Some cases cost over $100,000, especially if the injury is severe.

Standard Insurance Limits

You may think your homeowners insurance covers every pet incident. Most policies offer $100,000 to $200,000 in personal liability coverage. Some go up to $1 million, but many have breed restrictions or exclude pets with a history of aggression. If your dog bites someone and the costs go beyond your policy limit, you pay the rest out of pocket. Medical bills and legal fees add up fast.

Note: Many standard policies do not cover all breeds or repeated incidents. You could face big gaps in protection.

Added Security

You can protect your savings and home with an umbrella policy. This extra layer of coverage gives you peace of mind:

Extends liability protection beyond your homeowners policy limits.

Covers medical bills, legal defense, and settlements for pet-related injuries.

Helps with claims that exceed $200,000 or $300,000.

Fills gaps if your standard policy excludes certain breeds or incidents.

Shields your assets from large lawsuits.

🐾 Don’t let one accident put your financial future at risk. Choose umbrella insurance and feel confident every time your pet greets a guest or neighbor.

5. Entertaining Guests

Accidents at Home

When you have people over, you want them to have fun. But accidents can happen quickly. A guest could slip on a wet floor. Someone might trip over a rug and fall. A person could get burned at a bonfire outside. Sometimes, a dog may bite someone visiting your house. A child could get hurt near the pool. Someone might even break something valuable in your home. These things are common at parties or gatherings.

Dog bites or attacks

Backyard pool injuries

Burns from bonfires or grills

Broken or damaged property

You might not think these things will happen. But they can happen at any party, big or small.

Liability Coverage

Homeowners insurance helps with many of these accidents. It usually pays for medical bills and repairs if you are at fault. But most policies have a limit, like $100,000 to $500,000. The average claim from a home party is about $26,175. Some lawsuits can cost much more. If a guest gets badly hurt and sues for more than your policy covers, you could owe a lot of money.

Note: Homeowners insurance often does not cover alcohol-related accidents or big parties. You may not have as much protection as you think.

Umbrella Policy Benefit

An umbrella policy can help protect your money and give you peace of mind. This extra coverage helps when a claim is bigger than your homeowners insurance. It pays for medical bills, legal costs, and damages over your main policy. For example, if a guest sues for $500,000 and your insurance only pays $300,000, the umbrella policy pays the rest. You keep your money safe and avoid stress. Hosting should be fun, not scary. An umbrella policy lets you invite guests without worry.

6. Pools and Trampolines

Injury Risk

Pools and trampolines are fun in your backyard. But they can be dangerous. Kids like to swim and jump. Accidents can happen very quickly. A child might slip on wet ground. Someone could fall off a trampoline. Even if adults watch, kids can get hurt. Broken bones and head injuries can happen fast. Drowning is also a risk. These accidents can cost a lot of money. You might have to pay for medical bills. If a neighbor’s child gets hurt, you could be blamed.

Insurance Exclusions

Homeowners insurance does not always cover these risks. Insurance companies call pools and trampolines “attractive nuisances.” This means they are fun but risky for kids. Here are some things to know:

Some insurance will not cover trampolines at all.

Pools can make your insurance cost more.

You may need a fence or safety net for coverage.

Injuries from pools or trampolines are often not covered unless you buy more protection.

Some companies will not insure homes with trampolines or hot tubs, even if you have a fence.

Tip: Always read your insurance policy. Check for rules and what is not covered before getting a pool or trampoline.

Extra Liability

Umbrella insurance gives you more protection than regular insurance. It gives you higher coverage and helps pay for lawyers. You can feel safer with this extra help. Here is how umbrella insurance helps:

Benefit | How It Protects You |

|---|---|

Excess Liability | Pays $1 million or more above your homeowners policy for pool and trampoline injuries. |

Legal Defense | Pays for lawyers and court costs if someone sues you after an accident. |

Cost Effective | Gives strong protection for a small yearly cost—often less than $1 a day. |

Safety Requirements | You must tell your insurer about pools or trampolines and follow safety rules. |

You cannot stop every accident. But you can be ready. Umbrella insurance helps protect your home, money, and future from pool and trampoline risks.

7. Volunteering

Community Activities

You want to help people in your town. You might coach a kids’ team or serve food at a shelter. You could join a group that helps make decisions. These things are good for your community. But they can have risks you might not think about. When you volunteer, you could get into legal trouble if something bad happens. Here are some examples:

Someone gets hurt at an event you help with.

You give advice or help outside your main job.

You work with kids or adults who need extra care.

Nonprofits try to keep everyone safe. They use background checks and give training. They write clear rules for what you should do. They also buy special insurance for volunteers. But normal insurance does not always cover everything. There are gaps, like when you help at a different place or use your own car.

Personal Liability

You might think the group’s insurance will protect you. But many times, it does not help volunteers. Business insurance usually covers workers, not helpers. You may not get workers’ compensation if you get hurt. If you drive your own car for a charity, your car insurance may not help. Some risks are:

Lawsuits if you make a mistake

Accidents during after-hours or at another location

You could owe a lot of money if someone sues you for an accident.

Peace of Mind

Umbrella insurance helps you feel safe when you help others. This policy gives extra protection when other insurance is not enough. It pays for legal bills, damages, and claims over your home or car policy. You can coach, volunteer, or join events without worrying about losing your money.

Umbrella insurance protects your money and your future. You can help others and not worry about surprise lawsuits. Give back to your community and know you have strong coverage.

You deal with risks all the time. Around one out of three Americans do not have enough liability coverage. Many people get an umbrella policy for more protection. It also helps pay for lawyers if you get sued. This makes people feel safer. Look at what you need. Talk to someone who knows about insurance. Think about getting this policy to keep your future safe.

FAQ

How much umbrella insurance do you need?

Pick coverage that matches what you own and your risks. Many people pick $1 million or more. More coverage means you get better protection.

Does umbrella insurance cover rental properties?

Yes, umbrella insurance can help if someone gets hurt at your rental property. You must add the property to your policy to get this coverage.

Can you buy umbrella insurance without home or auto insurance?

No, you must have a home or auto policy first. Umbrella insurance gives extra protection on top of your current coverage.